When it comes to keeping track of financial records, bookkeepers and accountants are like cameramen on a film crew. They each have different skills and knowledge of the various processes and techniques involved in filming, but the director is concerned with higher-level tasks. The company's bookkeeper is responsible to maintain its books. The accountant, on the other hand, is responsible for assessing the company's financial situation. Here are some things to consider when choosing between the two professions.

Accounting

A bookkeeper's job is to maintain your financial records and create reports for you. The accountant, on the other hand, has a broader perspective and tends to perform tasks such as planning and budgeting. Both types can be beneficial to a business' financial health. The accountant, however, is responsible for higher-level tasks and tends to concentrate on one area. Bookkeepers tend to be less expensive than accountants but they charge more per hour.

Payroll

Payroll bookkeepers perform similar job duties to accountants. Both occupations are expected to see job growth over several years. The Bureau of Labor Statistics predicts 4% job growth for accountants over the next decade. The demand for bookkeepers will decrease by 6%, however. Both types of accountants will be challenged by automation and new technology. Payroll bookkeepers should be aware of these issues and make sure that they have the appropriate education and experience.

Cash flow management

There is some overlap in bookkeeping and cash flow management tasks, but you might want to have both professionals working together. Your accountant can help you with payroll, which becomes more complicated once you hire employees. A bookkeeper can assist you in managing your cash flow. Both roles will give you insight and help manage your finances efficiently. But there are key differences. Read on to find out how bookkeeping can benefit your business.

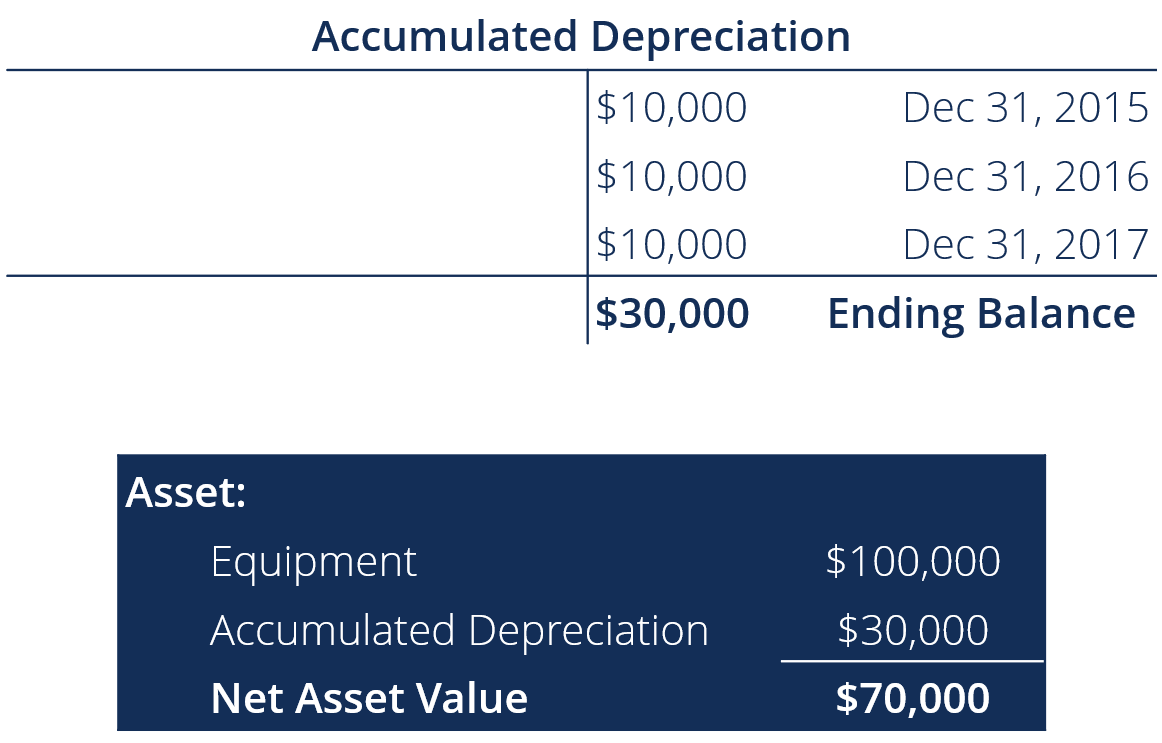

Balance sheet

There is a slight overlap of the roles and responsibilities of a bookkeeper versus an accountant. The former has all administrative responsibilities, while accounting is more advisory. Regardless of the role they play, bookkeepers and accountants are essential to all enterprises. Bookkeepers keep the company's financial records, but accountants can see the bigger picture and understand taxation rules.

Income statement

The key difference between an accountant-prepared income statement and a bookkeeper's is the accuracy of the financial statements. The income statement is calculated based upon the financial position. The net income of the company is used to calculate the balance sheet. The statement of operations is used to calculate the balance. Both statements are required by SEC as they contain important categories of information. An accountant must provide an explanation of mergers or acquisitions when a business merges with another entity.

FAQ

What is bookkeeping?

Bookkeeping is the art of keeping records of financial transactions for individuals, businesses, and organizations. It includes all business expenses and income.

All financial information is kept track by bookkeepers. These include receipts. Invoices. Bills. Payments. Deposits. Interest earned on investments. They also prepare tax reports and other reports.

What are the salaries of accountants?

Yes, accountants usually get paid hourly rates.

Complicated financial statements can be a charge for some accountants.

Sometimes accountants are hired to perform specific tasks. For example, a public relations firm might hire an accountant to prepare a report showing how well their client is doing.

Why is reconciliation so important?

It's important, as mistakes are possible at any moment. Mistakes include incorrect entries, missing entries, duplicate entries, etc.

These problems could have severe consequences, such as incorrect financial statements, missed deadlines or overspending.

What are the types of bookkeeping software?

There are three types of bookkeeping systems available: computerized, manual and hybrid.

Manual bookkeeping is the use of pen and paper to keep records. This method requires attention to every detail.

Computerized bookkeeping uses software programs to manage finances. It saves time and effort.

Hybrid bookkeeping is a combination of both computerized and manual methods.

Statistics

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- "Durham Technical Community College reported that the most difficult part of their job was not maintaining financial records, which accounted for 50 percent of their time. (kpmgspark.com)

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

External Links

How To

Accounting for Small Business

Accounting for small businesses is one of the most important tasks in managing any business. Accounting includes the preparation of financial reports and income statements, as well tracking expenses and income. It also involves the use of various software programs such as Quickbooks Online. There are many different ways you can do your small business accounting. You need to choose the most appropriate method for your business. Below we have listed some of the top methods for you to consider.

-

Use the paper accounting system. You might prefer to use paper accounting, which can be very simple. This method is very simple. You simply need to record transactions every day. If you are looking to ensure that your records are accurate and complete, you may want to consider QuickBooks Online.

-

Online accounting. Online accounting is a way to have easy access to your accounts no matter where you are. Wave Systems, Freshbooks and Xero are all popular choices. These software can be used to manage your finances, pay bills and send invoices. You can also generate reports. These programs offer many features and benefits. They also make it easy to use. These programs are a great way to save time and cash on your accounting.

-

Use cloud accounting. Another option you have is cloud accounting. It allows you to store your data securely on a remote server. Cloud accounting has many advantages when compared to traditional accounting software. Cloud accounting isn't dependent on expensive software or hardware. Because all your information is stored remotely, it provides better security. It eliminates the need to back up your data. It makes it easy to share files with others.

-

Use bookkeeping software. Bookkeeping software can be used in the same manner as cloud accounting. But, it is necessary to purchase a new computer and install it. Once you have installed the software, the software will allow you to connect to the Internet so you can access your accounts whenever it suits you. You will also have the ability to access your accounts and balances directly from your PC.

-

Use spreadsheets. Spreadsheets enable you to manually enter your financial transactions. For example, you can create a spreadsheet where you can enter your sales figures per day. A spreadsheet's advantage is that you can make changes to them at any time without having to change the whole document.

-

Use a cash book. A cashbook lets you keep track of every transaction. Cashbooks come in different sizes and shapes depending on how much space you have available. You can either use a separate notebook for each month or use a single notebook that spans multiple months.

-

Use a check register. Check registers are a tool that allows you to organize receipts and payment information. To transfer items to your check list, all you have to do is scan them in your scanner. To help you remember what was bought, you can make notes once you have scanned the items.

-

Use a journal. A journal is a type logbook that tracks your expenses. This is best for those who have recurring expenses like rent, insurance, and utilities.

-

Use a diary. A diary is simply a journal that you write to yourself. You can use it to keep track of your spending habits and plan your budget.