In business, a bookkeeper performs various tasks. They prepare bank and credit card statements for customers and reconcile them. They reconcile the bank and credit card statements, as well as create invoices for customers. Bookkeepers also provide financial reports on a regular basis. In addition, they keep track of receipts.

Send invoices promptly

If you want to avoid being late with payments, make sure your invoices are sent promptly. This will increase your chances of receiving payment. Depending on your business's size, an automatic invoice processing program may be an option. It eliminates the need for manual checks and increases the likelihood of receiving payment. Automated invoices are faster and more economical than manual invoice processing.

Automated software allows you to automatically send invoices the accounts payable department. Some systems will alert you when an invoice is viewed or opened. Before you send invoices, double-check that the automated system you use is working correctly. Invoices that have not been viewed should be checked regularly in your email. It's a sign that the invoice has not reached the right people if they aren't viewed. Automated systems will alert you if you haven't viewed an invoice. This will make sure that you don't miss out on the opportunity to receive payment.

Consolidate all balance sheet accounts in order to verify that the amounts are correct

Balance sheet reconciliation is an important part of the accounting process. It helps you spot duplicate or missing transactions. Also, it can help with tracking various regulatory compliance items. Standard templates can simplify the process. These templates can be saved in a shared drive or centralized repository. They allow for consistency and easy review. Before implementing a reconciliation, you should first understand the composition of the accounts you plan to reconcile. If you have a cash balance, you'll want to reconcile it with your general ledger or bank statement.

If a company keeps track of each transaction, it's crucial to reconcile all balance account accounts to ensure accurate amounts. This includes bank accounts, fixed assets and accumulated deduction. Reconciliation of these accounts is important for the growth of a business, so it's critical to have the correct information available.

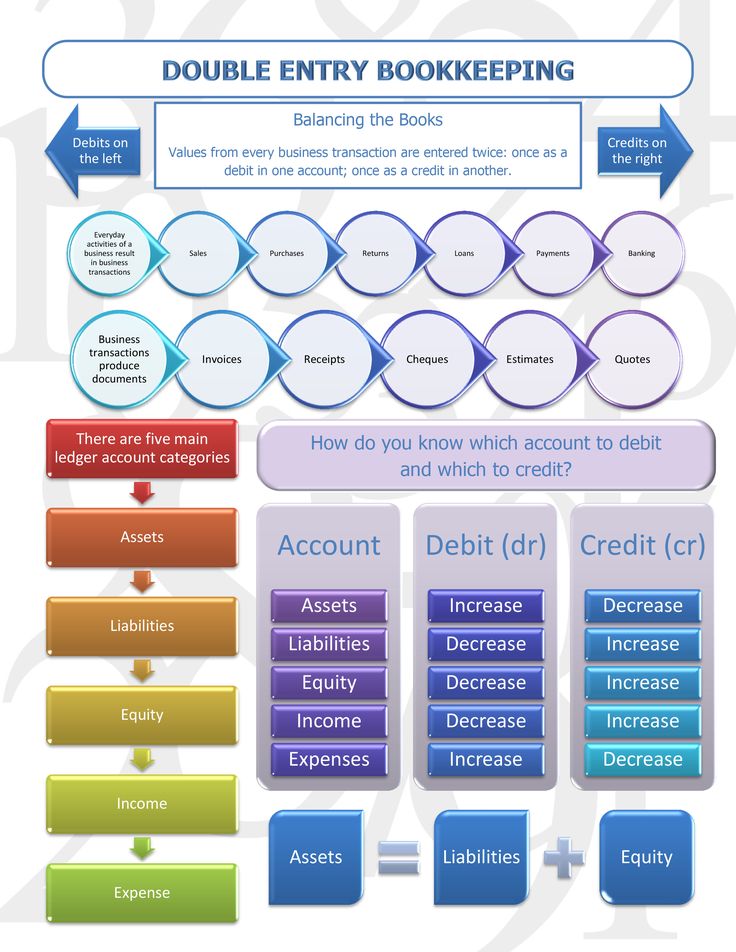

Provide regular financial reports

Bookkeepers prepare financial reports for small businesses. They include a profit statement, balancesheet, and cash flow statements. These financial reports allow you to assess your business's financial health and show how profitable your business is. They also assist employees with their payroll taxes. They can also handle foreign currency accounts. Modern bookkeeping software allows for quick analysis of exchange rates.

You can see the financial health of your company by reviewing accounts payable and receivable statements. These reports will show you the total money owed to customers and suppliers. These reports also include the due dates of payments. These reports give you a good idea of how profitable your company is. This can have an impact on your spending.

Manage receipts

A bookkeeper manages receipts to maintain a business's financial records. This includes documenting all business transactions in a timely fashion. This data is then transferred to the accounting journal at the end of each month. There are several tools to assist bookkeepers in this process.

Receipts on paper can be difficult to keep track of and easily lose. Environmental factors can also cause them to be damaged. It can also be difficult to find and organize them. Handling receipts is time-consuming and difficult to track. Luckily, there are several apps available for managing receipts, both online and on mobile devices.

FAQ

What's the difference between accounting & bookkeeping?

Accounting is the study of financial transactions. The recording of these transactions is called bookkeeping.

They are both related, but different activities.

Accounting deals primarily in numbers while bookkeeping deals with people.

For reporting purposes on an organization's financial condition, bookkeepers keep financial records.

They ensure that all the books are balanced by correcting entries for accounts payable, accounts receivable or payroll.

Accounting professionals examine financial statements to determine if they are in compliance with generally accepted accounting principles.

They may suggest changes to GAAP if they do not agree.

So that accountants can analyze the data, bookkeepers keep records about financial transactions.

What is an auditor?

Auditors look for inconsistencies among the financial statements' information and the actual events.

He confirms the accuracy and completeness of the information provided by the company.

He also checks the validity of financial statements.

What is an accountant and why are they so important?

An accountant keeps track and records all the money you spend and earn. They also record how much tax you pay and what deductions are allowable.

An accountant helps manage your finances by keeping track of your income and expenses.

They prepare financial reports for individuals and businesses.

Accountants are essential because they need to understand everything about numbers.

In addition, accountants help people file taxes and ensure they're paying as little tax as possible.

Statistics

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- Employment of accountants and auditors is projected to grow four percent through 2029, according to the BLS—a rate of growth that is about average for all occupations nationwide.1 (rasmussen.edu)

- The U.S. Bureau of Labor Statistics (BLS) projects an additional 96,000 positions for accountants and auditors between 2020 and 2030, representing job growth of 7%. (onlinemasters.ohio.edu)

- According to the BLS, accounting and auditing professionals reported a 2020 median annual salary of $73,560, which is nearly double that of the national average earnings for all workers.1 (rasmussen.edu)

External Links

How To

How to become an accountant

Accounting is the science of recording transactions, and analysing financial data. It can also involve the preparation statements and reports for various purposes.

A Certified Public Accountant (CPA), is someone who has passed a CPA exam and is licensed by the state boards of accounting.

An Accredited Financial Analyst (AFA), is someone who has met certain criteria set by the American Association of Individual Investors. The AAII requires that individuals have at least five years of investment experience before becoming an AFA. They must pass a series exam to verify their understanding of accounting principles.

A Chartered Professional Accountant (CPA), sometimes referred to as a chartered accountant, is a professional accountant who has been awarded a degree from a recognized university. CPAs need to meet the specific educational standards set forth by the Institute of Chartered Accountants of England & Wales.

A Certified Management Accountant (CMA), is a certified professional accountant that specializes in management accounting. CMAs need to pass exams administered through the ICAEW, and must continue education requirements throughout their careers.

A Certified General Accountant is a member of American Institute of Certified Public Accountants. CGAs are required to take several tests; one of these tests is known as the Uniform Certification Examination (UCE).

The International Society of Cost Estimators offers the certification of Certified Information Systems Auditor (CIA). Candidates for the CIA certification must complete three levels, which include coursework, practical training and a final assessment.

Accredited Corporate Compliance officer (ACCO) is a distinction granted by the ACCO Foundation, and the International Organization of Securities Commissions. ACOs must possess a Bachelor's Degree in Finance, Business Administration, Economics, or Public Policy. They must pass two written exams, and one oral exam.

A credential issued by the National Association of State Boards of Accountancy is called a Certified Fraud Examiner. Candidates must pass three exams with a minimum score 70 percent.

International Federation of Accountants is accredited a Certified Internal Audior (CIA). The International Federation of Accountants (IFAC) requires that candidates pass four exams. These include topics such as auditing and risk assessment, fraud prevention or ethics, as well as compliance.

American Academy of Forensic Sciences (AAFS) designates an Associate in Forensic Account (AFE). AFEs must have graduated with a bachelor’s degree from an approved college or university in any other study area than accounting.

What does an auditor do exactly? Auditors are professionals who inspect financial reporting controls and audit the internal controls. Audits can be conducted randomly or based upon complaints from regulators regarding the organization's financial reports.